You’ve probably already done the exciting part. You found strong talent in the Philippines, priced out a seat-leasing setup, and realized the operating model can be far leaner than a traditional office launch. Then the tax questions showed up.

That’s usually where momentum slows. Foreign-owned startups and BPO operators don’t struggle because Philippine tax rules are impossible. They struggle because taxes in philippines affect almost every operating decision at once: entity setup, pricing, payroll handling, invoicing, cash flow, intercompany contracts, and recordkeeping.

The practical way to approach it is to stop treating tax as a year-end cleanup exercise. In this market, tax is part of your operating design. If you structure the business properly at the start, your finance team has fewer surprises, your monthly close is cleaner, and your seat-leasing savings don’t get eaten by avoidable compliance mistakes.

For day-to-day control, one of the least glamorous but most useful habits is getting bank activity into a workable format early. If your team needs a better way to manage bank data for tax season, that process matters more than most founders expect because messy transaction data often turns simple tax filings into expensive reconciliation work. If you’re evaluating the operational side of flexible workspace entry, the Philippine market setup options are worth reviewing alongside your tax planning so the commercial model and compliance model fit each other.

Your Starting Point for Philippine Tax Compliance

Most foreign entrants ask the wrong first question. They ask, “What tax rate applies to us?” The better question is, “What activities will trigger tax, who has to file, and which documents will support those filings?”

That shift matters because taxes in philippines aren’t just about rates. They’re about classification. A company with local staff, local invoices, service revenue, related-party charges, and a flexible office footprint can have several parallel obligations running at the same time. If you only focus on the headline rates, you’ll miss the administrative burden that drives cost.

What usually causes trouble first

The first operational problems tend to come from four areas:

- Entity mismatch: The legal structure doesn’t match how revenue is earned or how headquarters funds local operations.

- Invoice timing: The finance team issues invoices without aligning them to filing and documentation requirements.

- Payroll handling: Employers underestimate the compliance role they play in withholding and remittance.

- Documentation gaps: Expenses are real, but the proof behind them is incomplete.

A tax-efficient launch starts by mapping your workflow before your first filing date arrives. That means identifying who signs contracts, who hires staff, who bills clients, where cash is collected, and whether local functions support affiliates or unrelated third parties.

Practical rule: If a transaction can’t be explained clearly by operations, it usually becomes harder to defend in tax.

The right mindset for market entry

The Philippine system rewards businesses that stay organized. It’s less forgiving to businesses that improvise month by month.

For startups and BPO teams, that means building a repeatable compliance rhythm from the beginning. Don’t wait until annual reporting to discover that service agreements are vague, payroll records don’t reconcile to accounting, or intercompany charges were never documented properly. The businesses that keep costs under control aren’t always the ones paying the lowest tax. They’re often the ones avoiding rework, penalties, disputed deductions, and management distraction.

The Philippine Tax Landscape Demystified

A foreign-owned BPO can sign a lease, hire its first team, and start serving clients within weeks. The tax exposure starts just as fast. In practice, the early cost overruns usually come from classification errors, permit delays, and filing gaps that could have been avoided with a clearer view of how the Philippine system is split between national taxes and local business requirements.

At the national level, the Bureau of Internal Revenue oversees the taxes that affect revenue recognition, invoicing, payroll withholding, and many outbound payments. At the local level, the city or municipality controls permits, local business taxes, and activity-based requirements tied to your office location. For a seat leasing operator, this split affects more than paperwork. It shapes where you can operate, what you can bill from that site, and how easily you can renew without disrupting client delivery.

Tax policy also shifts over time, and those changes can alter pricing and registration decisions. Reforms under the TRAIN Law increased the VAT threshold to ₱3 million in annual sales while keeping the standard VAT rate at 12%, as summarized by Philippines tax revenue data. For founders comparing service models, the Seat Leasing BPO industry blog is a useful reference for the commercial implications of those rules.

National taxes versus local obligations

National taxes usually consume more management time because they run on a strict filing calendar and depend on accurate accounting support. Income tax, VAT, percentage tax where applicable, documentary stamp tax in certain transactions, and withholding taxes all sit in this category. If your finance team misses the character of a transaction, the result is often a wrong filing position, a denied deduction, or avoidable exposure during audit.

Local obligations have a different operational effect. They determine whether the business is properly licensed in the city where staff work, whether declared activities match its service model, and whether annual renewals proceed without friction. I often see BPO entrants focus on BIR registration first and treat city hall compliance as an admin task. That approach becomes expensive once lease details, headcount, floor use, and declared business activities stop matching across records.

Direct taxes versus indirect taxes

A second distinction helps with budgeting and contract design. Some taxes reduce profit directly. Others pass through the transaction cycle but still create cash flow pressure and control requirements.

Income tax is the clearest direct tax for most companies. VAT is the clearest indirect tax. Withholding taxes sit in a separate practical category because the Philippine entity may be responsible for collecting or remitting tax on payments even when the tax does not belong to the company economically.

For BPOs and seat leasing businesses, that difference affects day-to-day decisions:

- Direct taxes influence margin, transfer pricing support, and year-end profitability.

- Indirect taxes influence client pricing, invoice format, and the timing gap between collections and remittance.

- Withholding taxes influence vendor onboarding, contract wording, and the release of payments.

A small tax amount can still create a large operating problem if it blocks a deduction, delays a permit renewal, or forces the finance team to reconstruct support documents months later.

Why this matters for BPO and seat leasing models

Seat leasing and managed office setups often bundle rent, internet, utilities, staffing support, and administrative services into one operating model. That is commercially attractive, but it can blur the tax treatment of each charge if contracts and invoices are drafted too loosely. The more bundled the arrangement, the more discipline you need in classifying revenue, documenting support services, and matching the legal form to what happens on the floor.

For this reason, taxes in the Philippines should be handled as part of operating design from the start. A business that knows which obligations sit with the BIR, which sit with the local government, and which payments trigger withholding can price more accurately, protect deductions, and avoid the quiet compliance costs that erode margin in the first year.

Key Business Taxes You Must Know

A foreign-owned BPO can price a contract correctly and still miss its margin in the first year if tax was treated as a filing issue instead of an operating cost. I see this often with seat leasing and managed office models. Revenue looks healthy on paper, but VAT timing, payroll withholding, and weak support for deductions push cash out faster than management expected.

Three tax areas usually drive that outcome: corporate income tax, VAT, and withholding taxes. Each one affects a different part of the business. Corporate income tax affects retained profit. VAT affects billing and cash timing. Withholding affects how money leaves the company, whether through payroll or vendor payments.

Corporate income tax

Corporate income tax is the tax management watches at year-end, but the work that protects the tax position happens much earlier. For BPOs and seat leasing operators, the practical question is whether the Philippine entity’s books match what the business is doing on the ground.

If the local company hires staff, occupies office space, delivers support services, and contracts with customers, those facts should line up with the accounting records, intercompany charges, and legal documents. If they do not, the tax cost is rarely limited to a year-end adjustment. It can affect deductibility, transfer pricing support, and the amount of time finance leadership spends defending ordinary business expenses.

This is also where operating design matters. A provider offering bundled office space, connectivity, utilities, and admin support needs contracts and invoices that clearly reflect those service components. Reviewing typical seat leasing inclusions and support services helps management see where tax classification can drift away from the commercial model if documentation is too broad or too vague.

VAT

VAT affects pricing discipline more than many new entrants expect. A business can remain profitable on paper and still feel strain if output VAT must be reported before customer collections come in.

For BPO and seat leasing businesses, that timing issue is practical, not theoretical. Long client payment terms, upfront fit-out costs, and recurring utility charges can create a funding gap between invoicing and collection. Finance teams should therefore look at VAT together with contract terms, billing cycles, and collection performance. If those pieces are handled separately, the business often ends up financing tax out of working capital.

Registration status also matters. Once the business reaches the point where VAT applies, invoice form, supporting documents, and input VAT tracking need to be handled with consistency. Errors here usually show up later, when the company tries to support claims or explain differences between sales records and filed returns.

Withholding taxes and payroll handling

Withholding taxes create some of the most frequent compliance mistakes because the company is acting as collector and remitter, not just taxpayer. That applies to employee compensation and to certain vendor and service payments.

For foreign-owned groups, payroll withholding deserves close supervision from the start. Senior hires, shift differentials, allowances, bonuses, and other compensation items need to be classified correctly before payroll runs become routine. Once errors repeat over several months, cleanup becomes expensive and distracting. The tax itself may sit with the employee in principle, but assessment risk, penalties, and document problems usually land on the employer.

Vendor payments raise a similar issue. If the business pays rent, professional fees, contractors, or service providers without checking withholding obligations first, the payment process becomes the weak point. I generally advise clients to build tax review into accounts payable approval, especially in BPO setups where recurring outsourced services are common.

Operational takeaway: In the Philippines, withholding mistakes usually start as a process failure, not a tax law problem.

Comparison of Major Business Taxes

| Tax Type | Typical Business Impact | Tax Base | Typical Filing Frequency |

|---|---|---|---|

| Corporate Income Tax | Affects net margin, deductibility, and support for intercompany pricing | Corporate taxable income | Quarterly and annual, depending on filing obligations |

| VAT | Affects client pricing, invoicing, and working capital timing | Taxable sales of goods or services, subject to registration status | Periodic filings based on applicable compliance cycle |

| Withholding on compensation and certain payments | Affects payroll accuracy, vendor payment processing, and assessment exposure | Employee compensation and qualifying payments to vendors or service providers | Regular remittance during the year, with annual or periodic reconciliation |

What works in practice

The strongest tax setups are usually operationally simple.

- A clean chart of accounts: Revenue streams, payroll, occupancy costs, and intercompany charges should be easy to trace and explain.

- Invoice discipline: Contracts, invoices, and receipts should support the same tax treatment.

- Monthly reconciliations: Reconcile accounting records, payroll reports, and tax filings before issues accumulate.

- Controlled payment approvals: One accountable finance lead should review tax treatment before payroll is finalized or major payments are released.

What doesn’t work

Weak setups usually share the same pattern. Operations agree commercial terms. Finance records the transaction later. Tax review happens after payment, often with incomplete documents and inconsistent descriptions across contracts, invoices, and ledger entries.

That approach raises compliance costs quickly. Corrections consume management time, delay filings, complicate audits, and make ordinary deductions harder to defend. For BPOs and seat leasing clients operating on tight margins, those hidden costs matter as much as the headline tax rates.

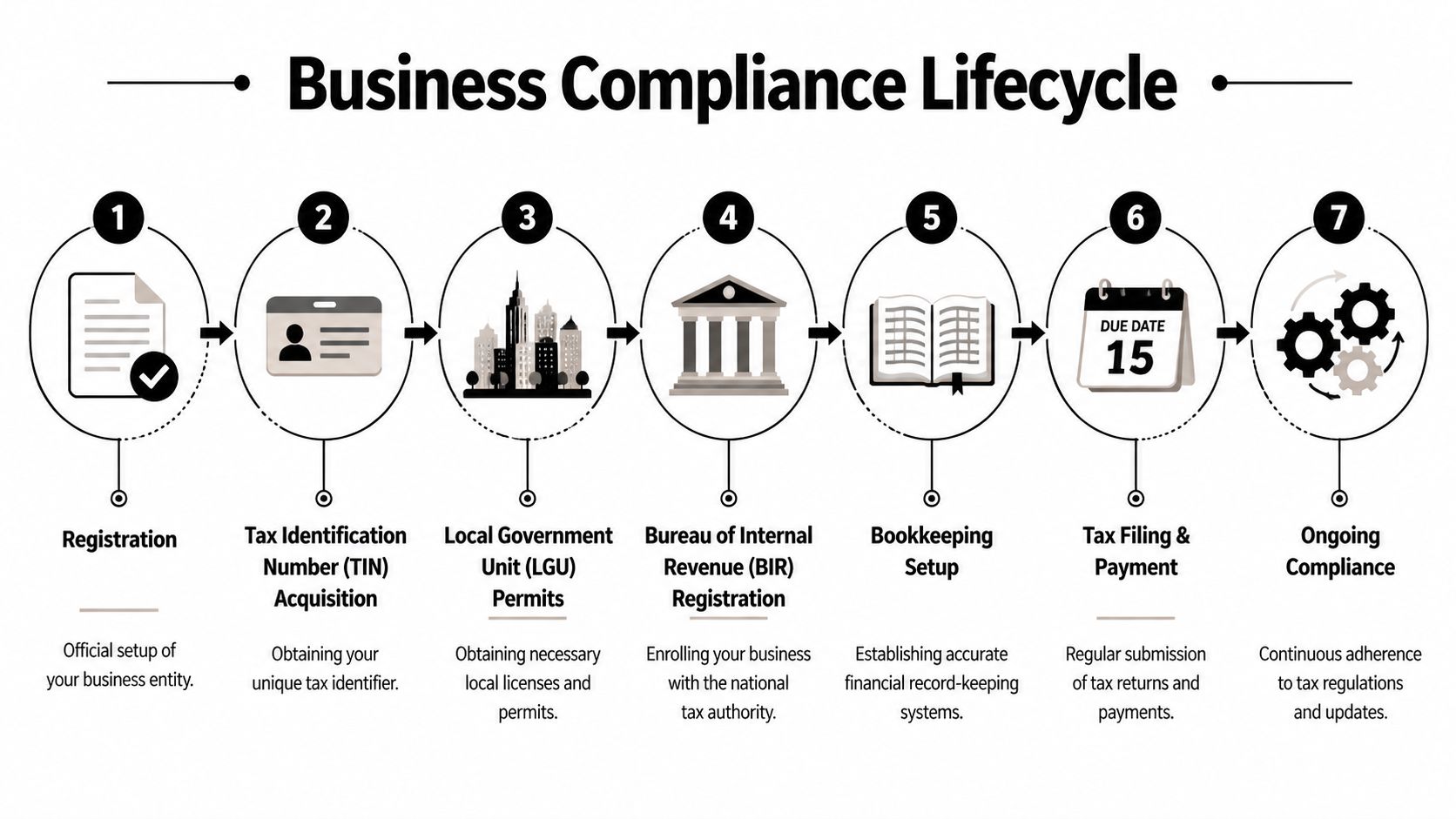

The Business Compliance Lifecycle From Registration to Filing

A business that handles taxes well in the Philippines usually follows a repeatable cycle. The sequence matters because later filings depend on earlier registrations, classifications, and bookkeeping decisions.

If you’re assessing what’s bundled operationally in a flexible office model, the workspace support inclusions are useful to review because tax compliance works better when responsibility for utilities, IT, connectivity, and support services is already clear in the commercial arrangement.

Step one through four

The front end of compliance is administrative, but it shapes everything that follows.

Register the business entity

Your corporate form and business purpose should match what the company will do in the Philippines.Secure a Tax Identification Number

This is foundational. Without it, filings and official tax transactions stall quickly.Obtain local permits

Local government requirements aren’t just paperwork. They support operational legitimacy and need to be kept in step with actual business activity.Complete BIR registration

With BIR registration, tax obligations become active in a practical sense. Your registration profile drives what the business is expected to file.

Step five through seven

Once registration is complete, the more important discipline begins.

Set up bookkeeping correctly

Use an accounting system that can separate revenue streams, payroll costs, taxes withheld, and related-party transactions. QuickBooks, Xero, and NetSuite can all work if the account mapping is done properly. The software isn’t the solution by itself. The logic behind the setup is.File and pay on schedule

Businesses that file accurately but late still create avoidable exposure. The finance team should know which returns recur monthly, quarterly, and annually.Maintain ongoing compliance

Tax compliance is continuous. Registrations change, business lines evolve, and staff headcount grows. Your controls need to keep up.

Good compliance systems are boring by design. If your tax process depends on heroics every deadline week, the process is weak.

A practical monthly routine

For BPO operators and foreign-backed startups, the smoothest workflow usually looks like this:

- Week one: Close books for the prior period and reconcile bank activity.

- Week two: Review payroll, contractor payments, and tax withholdings.

- Week three: Finalize returns, supporting schedules, and payment approvals.

- Week four: Archive documents, investigate mismatches, and update trackers.

This works because it turns tax into an operations calendar rather than a panic event.

Where businesses usually lose control

The most common compliance failure isn’t ignorance of a tax rule. It’s poor handoff between teams. HR runs payroll, operations approves vendors, accounting books expenses, and an external preparer files returns. If nobody owns the full sequence, filings may technically go out, but they won’t always reconcile.

That’s why one accountable finance owner matters. Even with outsourced help, someone inside the business should understand what was filed, why it was filed that way, and which source documents support it.

Tax Strategies for BPOs and Seat Leasing Clients

A foreign-owned BPO can look profitable on paper and still bleed cash in the first year because the tax setup does not match the operating model. I see this often with seat-leasing entrants. They sign a facility package, hire quickly, start billing offshore affiliates, and only later realize their invoicing, withholding, and transfer pricing support do not line up.

The better approach is to build the tax position around how money moves through the business. For BPOs, seat-leasing operators, and foreign groups testing the Philippine market, that usually means paying close attention to revenue classification, cost recovery, intercompany pricing, and document control from day one.

The 8% regime for qualifying small operators

For solo professionals and very small service providers around the BPO sector, the 8% option can reduce compliance work and make tax cost more predictable. It is often relevant to independent consultants, small recruitment support firms, trainers, and early-stage service operators that have straightforward receipts and limited overhead.

As noted earlier, qualifying taxpayers below the applicable threshold may elect the 8% regime instead of the usual graduated income tax approach plus percentage tax. The practical benefit is not just a simpler return. It also reduces time spent defending deductions, splitting mixed expenses, and cleaning up bookkeeping errors at filing time.

That said, low admin burden does not automatically mean lower tax. A business with meaningful payroll, software, subcontractor, or occupancy costs may be better off under the regular regime if those deductions materially reduce taxable income. For small operators in this space, the right comparison is simple: measure tax payable under both methods and include the compliance cost of each, not just the headline rate.

Why seat-leasing clients should think beyond rent

Seat leasing affects tax far beyond office occupancy. In practice, it shapes how the Philippine entity proves what it is paying for, what it is reselling, and which charges belong to core operations versus support.

That distinction matters.

A bundled seat-leasing agreement may include workstation use, internet, IT support, security, reception, utilities, HR assistance, or management services. If finance books everything as “rent,” the company may have trouble explaining the cost base for client billing, defending deductions, or supporting affiliate recharges. A cleaner setup separates the components and matches them to contracts, invoices, and actual use.

For BPOs, this also improves pricing discipline. Management can see the actual cost per productive seat, the markup on client-facing services, and the hidden overhead that erodes margin.

Useful documentation usually includes:

- separate schedules for facility charges, technology support, and admin services

- contracts that match the actual services delivered on site

- invoice descriptions that are specific enough for audit review

- records showing how shared costs were allocated across teams or affiliates

- a retention policy for support files, including guidance on how long to retain business documents

Clean documentation often saves more money than aggressive tax positions because it protects deductions and shortens audit disputes.

Transfer pricing for multinational groups

Transfer pricing is where many foreign-backed BPO structures become expensive to fix. If the Philippine company provides support services to a parent or affiliate abroad, the tax team needs to prove what functions are performed locally, which risks are borne in the Philippines, and how the service fee or markup was set.

This issue comes up constantly in BPO and seat-leasing models. The Philippine entity may handle customer care, finance operations, technical support, recruitment, or back-office processing for a related company. If contracts say “strategic services” but the local team mainly performs routine support work, the documentation invites scrutiny. If the markup is copied from another jurisdiction without local analysis, that also creates risk.

What works in practice:

- intercompany agreements drafted for the Philippine facts, not copied from another country

- a clear description of the local entity’s functions, assets, and risks

- cost pools that exclude non-chargeable or poorly supported items

- invoicing and accounting treatment that match the contract terms

- support prepared while the year is still open, not after questions arrive

What usually fails:

- generic service descriptions

- markups with no basis in the actual service profile

- related-party charges booked late with weak support

- staff activity that does not match the paper trail

A short explainer can help your internal team align on the business side before the tax file is prepared.

A decision framework that saves time

For BPO and seat-leasing businesses, three early decisions usually drive the long-term tax outcome.

Who is the Philippine entity really serving?

Third-party billing, affiliate support, and mixed models each create different risks around invoicing, VAT treatment, and transfer pricing support.Is the business model light enough for simplified treatment, or is it already carrying a full operating cost base?

That choice affects both tax payable and finance headcount pressure.Can each major payment stream be traced from contract to invoice to ledger to return?

If the answer is no, the business is already carrying unnecessary tax risk.

The strongest operators in this sector treat tax as part of delivery economics. They price contracts with tax friction in mind, separate bundled costs before those costs become messy, and document related-party dealings before year-end pressure sets in. That is how a Philippine BPO or seat-leasing setup stays efficient as it scales.

Common Tax Pitfalls and How to Avoid Them

A lot of businesses assume tax risk comes from underpaying. In practice, plenty of tax problems start with poor systems, incomplete records, and casual assumptions that “we’ll sort it out at year-end.”

That approach fails quickly in the Philippines because the administrative burden is real. At the 2026 EODB Briefing, Mon Abrea highlighted that the Philippine tax system imposes high compliance costs, frequent audits, and delays in VAT refunds, conditions that can erode investor confidence and discourage MSMEs, as reported by BusinessWorld’s coverage of the overtaxed but underserved tax system.

Pitfall one through three

The first group of mistakes usually looks ordinary. That’s why it gets overlooked.

Missed deadlines

A return can be substantially correct and still trigger a problem if it’s filed or paid late. Deadline control should never depend on memory.Weak expense support

Finance teams often have genuine business expenses but poor supporting files. During review, unsupported expenses become hard to defend.Contractor and employee confusion

If a worker looks integrated into the business in practice, but is documented loosely, the tax and payroll consequences can become messy.

Pitfall four and five

These are the issues that often frustrate growing BPO operators the most.

VAT expectations that don’t match reality

Businesses sometimes assume VAT is just a formula. It isn’t. VAT also depends on registration status, invoice discipline, and document quality. Refund and recovery issues can become slow and admin-heavy, which is why cash flow planning matters as much as tax calculation.

Record retention treated as an afterthought

Recordkeeping sounds clerical until a question arises months later and no one can locate the support. A practical internal policy should cover contracts, invoices, proof of payment, payroll records, board approvals where relevant, and tax filings. If your team wants a plain-English benchmark for how long to retain business documents, use it to create a retention schedule that fits your accounting and legal workflow.

Paying the tax is only half the job. The other half is proving why the return was correct.

Controls that actually help

Businesses don’t need perfect systems on day one. They do need a few controls that are consistently followed.

- One filing calendar: Maintain a single source of truth for all recurring tax tasks.

- One document owner: Someone should be responsible for collecting support before filing, not after.

- One transaction review rule: Unusual payments, affiliate charges, and new compensation arrangements should be reviewed before processing.

- One archive method: Save records in a consistent folder structure, with naming conventions that make retrieval easy.

The trade-off most founders miss

Some founders try to minimize cost by keeping tax administration as lean as possible. That can work at very small scale. It stops working once you hire, invoice regularly, or deal with related parties.

The hidden cost of minimal compliance isn’t just penalties. It’s executive time. When management has to reconstruct transactions, explain mismatches, or answer avoidable queries, the business loses focus. In a BPO environment, that distraction shows up in client delivery, finance close quality, and expansion speed.

Building a Tax-Efficient Business in the Philippines

The practical answer to taxes in philippines is not to chase clever shortcuts. It’s to build a business that can explain its numbers clearly. When the legal setup, accounting records, payroll process, invoices, and contracts all match the actual operation, compliance becomes manageable.

For foreign-owned startups and BPOs, that usually means a few disciplined choices. Choose the right tax posture early. Keep bookkeeping clean from the first month. Review whether simplified options like the 8% regime apply where relevant. Treat transfer pricing as an operational document issue, not just a tax memo issue. And don’t let filing obligations drift into the background.

A final checklist worth following

- Align structure with reality: Your entity, contracts, and revenue model should tell the same story.

- Build around documents: If an expense or charge matters, preserve support while the transaction is fresh.

- Review workflows, not just rates: Many tax failures come from process breakdowns, not misunderstanding the law.

- Use better source records: Bank data, payroll reports, and invoice archives should be easy to search and reconcile.

- Digitize early: If your finance team still handles too many records manually, Matil's comprehensive OCR guide is a useful starting point for reducing document friction in payables, bookkeeping, and tax support files.

The businesses that do well here usually don’t have simpler rules. They have better internal discipline. That’s why Philippine tax compliance, while demanding, is still very workable for companies that treat it as part of operations instead of an afterthought.

If you’re entering the Philippine market and want a flexible workspace model that supports faster setup and lower overhead, Seat Leasing BPO is worth considering. Their seat-leasing approach can help startups, BPO teams, and growing companies launch quickly while keeping office infrastructure, support services, and operating costs under control.