When you're looking at a lease agreement, it's easy to get lost in the jargon. Let's break it down with a simple analogy. Think of an operating lease like renting a car for a weekend getaway. You use it, you pay for that usage, and then you hand back the keys with no strings attached.

A capital lease (which accountants now officially call a finance lease) is a completely different animal. It’s more like financing a car you intend to drive for the next five years, with the very real possibility of owning it when the term is up.

The Classic Dilemma: Renting vs. Owning

That fundamental difference—temporary use versus a path to ownership—is the key to understanding how these leases will affect your business's finances. This isn't just semantics; it changes how you report assets and liabilities on your balance sheet.

For a long time, companies loved operating leases for one big reason: they kept massive financial commitments "off the books." This accounting maneuver made a company's balance sheet look leaner and less debt-heavy, which was a huge plus when talking to lenders or investors. The problem was, it often painted an incomplete picture of a company's real financial obligations.

The New Rules of the Game

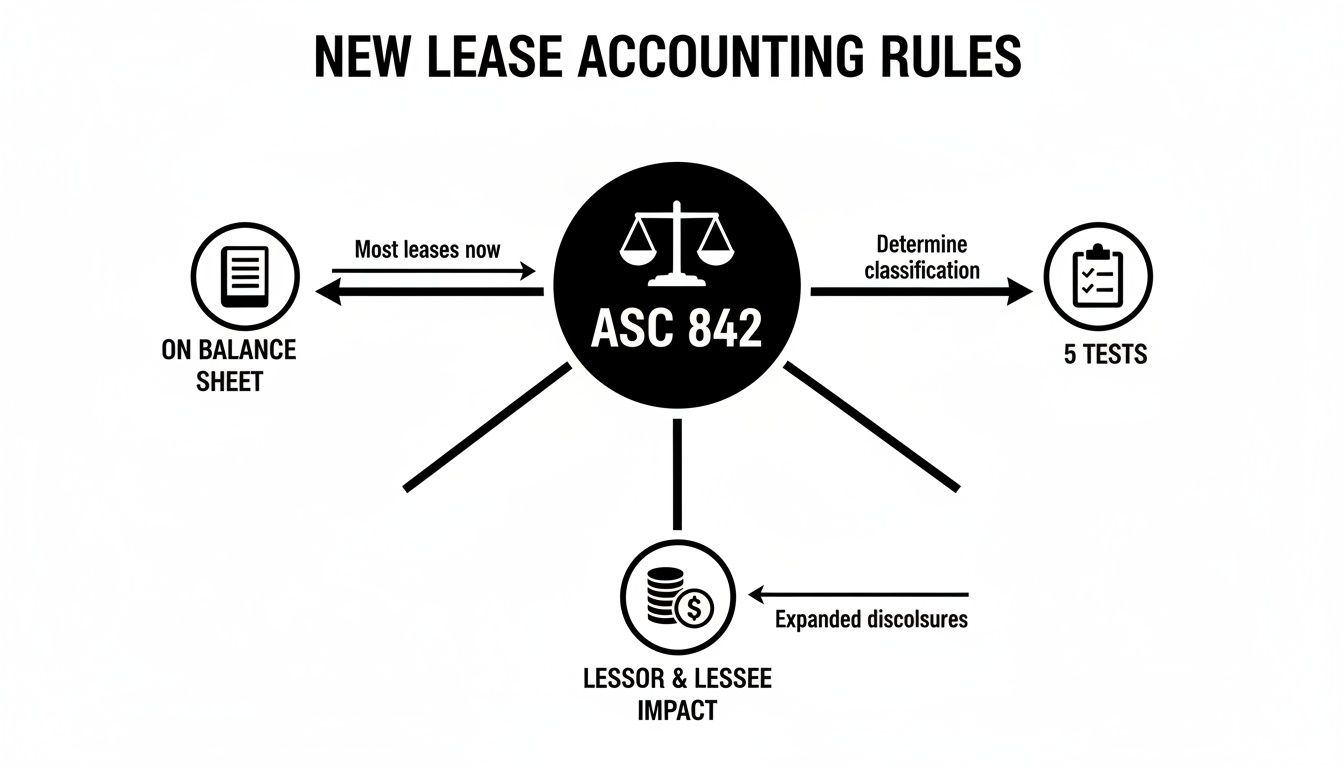

To pull back the curtain and give everyone a clearer view, accounting standards boards introduced some major changes: ASC 842 for U.S. companies and IFRS 16 for the rest of the world. The core of these new rules is that most leases, whether they're operating or finance, now have to be recognized on the balance sheet.

This was a massive shift with some serious consequences:

- Greater Transparency: Investors and banks can now see a company’s complete lease obligations, leaving no room for hidden debt.

- Altered Financial Ratios: Key performance indicators like debt-to-equity and asset turnover ratios are directly impacted, changing how a company's health is measured.

- More Strategic Decisions: The choice between lease types is no longer just an accounting exercise—it's a critical business strategy decision.

This isn't just boring accounting talk. It's a fundamental change in how your company tells its financial story, and it influences everything from your ability to get a loan to how attractive you look to potential investors.

Getting a handle on this new reality is crucial for any business leader. It's especially important in fast-moving industries where agility is everything. For example, a growing BPO that needs flexible office space might look to a provider like Seat Leasing BPO to find a workspace solution that works within these new accounting rules.

Understanding this framework is the first step toward making smarter, more strategic leasing decisions for your company.

Demystifying the New Lease Accounting Rules

Lease accounting used to be a lot simpler. Not long ago, companies could use something called an "operating lease" to keep huge financial commitments—like a ten-year office rental—completely off their main financial statements. This was common practice, often called off-balance-sheet financing, but it had a big downside: it could paint a misleading picture of a company's real financial health for investors and lenders.

That all changed with the rollout of two major accounting standards: ASC 842 for the U.S. and IFRS 16 for the rest of the world. Regulators put these new rules in place for one simple reason: transparency. The idea was to make sure a company's balance sheet tells the whole story of its long-term financial promises. Now, pretty much every lease has to be recorded on the books.

The Five-Point Checklist for a Finance Lease

So, how can you tell if your lease is what we now call a finance lease (the new term for a capital lease)? Accountants run it through a five-point test. If your lease agreement triggers just one of these five conditions, it’s officially a finance lease.

Think of these tests as a way to figure out if you're truly just "renting" or if the deal looks a lot more like a purchase. They get to the heart of who really benefits from the asset and who carries the risk.

Here are the five key questions to ask yourself:

- Ownership Transfer: Will the asset automatically become yours at the end of the lease?

- Bargain Purchase: Is there an option to buy the asset for a price so low it's a virtual certainty you'll take it?

- Lease Term: Does the lease last for the major part of the asset’s useful life? The general rule of thumb here is 75% or more.

- Present Value: Do your total lease payments add up to almost the entire fair market value of the asset? The threshold is typically 90% or more.

- Specialized Nature: Is the asset so custom-built for you that the owner would have no other use for it once your lease is up?

Let's say you lease a custom piece of manufacturing equipment. It has a ten-year lifespan, and your lease term is for eight of those years. Right there, you've hit the 75% mark. That lease is a finance lease, and you have to treat it that way on your books.

These changes are having a huge impact, especially in hot real estate markets. In fact, global office leasing activity recently hit a six-year high, and under these new standards, many companies are now forced to record those long-term office commitments as finance leases. This is a direct consequence of the push for greater financial clarity. You can find more insights on global real estate trends and how they tie into these new accounting rules.

Understanding how to classify your leases isn't just a job for the finance department anymore. It's essential knowledge for any business leader signing contracts, managing assets, or trying to tell a clear and honest financial story.

How Each Lease Type Shapes Your Financial Statements

Knowing the difference between a finance lease and an operating lease is more than just an accounting exercise—it tells a completely different story on your company’s financial statements. While modern accounting rules require both to show up on the balance sheet, the way they hit your profitability and cash flow metrics can be worlds apart. This is where the theoretical choice between a lease becomes a very practical reality for your bottom line.

Under the latest standards, both lease types create a Right-of-Use (ROU) asset and a matching lease liability on your balance sheet. In simple terms, you record the value of what you get to use (the asset) alongside your obligation to pay for it (the liability). This first step is the same for both, and it adds a welcome layer of transparency to a company’s true financial commitments.

The real divergence, however, happens on the income statement, where the expenses are recorded. This is the single most important distinction for any business leader to get their head around.

The infographic below gives a great visual of how new accounting rules, like ASC 842, have changed the game, forcing leases onto the balance sheet and requiring a specific set of tests for classification.

This map drives home a key point: the days of "off-balance-sheet" financing are over. Businesses now have to be much more strategic about how their leases are structured.

The Finance Lease Expense Profile

A finance lease breaks down the expense into two distinct parts, treating it much like a traditional loan. The result is a front-loaded expense curve.

- Amortization Expense: This is essentially the depreciation of your ROU asset. As it loses value over the lease term, you record it as an expense.

- Interest Expense: The lease liability is like a loan balance, and it accrues interest. Each payment you make goes toward paying down that interest and the principal.

Since the interest portion is always highest at the beginning when the liability is at its peak, your total expense is greater in the early years and tapers off over time. This can put a bigger dent in your net income right out of the gate.

The Operating Lease Expense Profile

An operating lease, on the other hand, keeps things incredibly simple. It combines everything into a single, straight-line lease expense that stays the same for the entire life of the lease.

This predictable, even expense makes an operating lease a dream for budgeting and financial forecasting. You know exactly what the cost will be month after month, year after year, completely avoiding the fluctuating expenses of a finance lease.

This difference has a direct impact on key performance metrics that investors and lenders scrutinize, like EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). With a finance lease, the interest and amortization costs are added back when calculating EBITDA. But the single operating lease expense is not added back, which can make your reported EBITDA look lower.

Finance Lease vs Operating Lease Financial Impact

Let's break down the different treatments in a simple, side-by-side comparison to see how they affect your core financial statements.

| Financial Statement | Finance Lease (Formerly Capital Lease) | Operating Lease |

|---|---|---|

| Balance Sheet | Records an ROU asset and a lease liability. | Records an ROU asset and a lease liability. |

| Income Statement | Recognizes separate amortization and interest expenses. | Recognizes a single, straight-line lease expense. |

| Cash Flow Statement | Principal payments are a financing outflow; interest is an operating outflow. | The entire lease payment is classified as an operating outflow. |

As you can see, the initial balance sheet impact is identical. But from there, the treatment on the income and cash flow statements creates two very different financial pictures.

Ultimately, choosing a lease structure isn’t just an accounting decision—it’s a strategic one that directly shapes how the financial world sees your company’s performance and stability.

When you're deciding between a capital or an operating lease, you're not just making a simple accounting choice. You're plugging into a massive global trend that’s reshaping how businesses manage their assets.

Companies everywhere are looking for smarter ways to grow without draining their bank accounts, and leasing has become the go-to solution. The equipment and real estate leasing market is booming for a reason.

The core appeal is simple: leasing gives you access to the mission-critical assets you need—from office buildings to IT hardware—without the huge upfront expense of buying them outright. For any business, cash is oxygen. This is especially true for startups and BPOs. Leasing keeps your cash free for what really matters: hiring talent, running marketing campaigns, and fueling your growth.

Why Leasing is More Than Just a Trend

In a world where things change in the blink of an eye, flexibility is your greatest weapon. Market demands shift, today's technology is tomorrow's relic, and your business strategy might need to pivot on a dime. Leasing is built for this reality.

When you lease, you avoid getting stuck with an asset that might not make sense for your business in a few years. It's this strategic agility that’s fueling the incredible growth in the leasing market.

This isn't just a fleeting fashion; it's a fundamental shift in how successful companies are built and scaled.

A Market on Fire

Just how big is this shift? In 2025, the global capital lease market was valued at an astonishing USD 2,084.78 billion. And it's not slowing down. Projections show it growing at a compound annual growth rate (CAGR) of 10% all the way through 2032, cementing its place as a cornerstone of modern business finance. If you want to dive deeper into the numbers, you can explore the full market analysis from Data Insights Market.

This growth isn't happening the same way everywhere. Different parts of the world have their own unique flavor:

- North America: Still the powerhouse, with deeply established leasing practices for everything from vehicles to heavy equipment.

- Europe: Leasing is a major driver here, especially within the industrial manufacturing and tech sectors.

- Asia Pacific: This region is seeing the fastest growth, powered by huge infrastructure development and a thriving BPO industry.

Seeing the bigger picture helps you realize that your leasing decision is part of a much larger economic story. Choosing the right capital operating lease structure isn't just about ticking a compliance box. It’s about aligning your business with powerful market forces to set yourself up for long-term success in a world that increasingly values access over ownership.

Making the Right Leasing Choice for Your Business

So, how do you translate all these accounting rules into a smart business decision? Choosing between a finance lease and an operating lease isn't just a box-ticking exercise for your accountant. It’s a strategic choice that can directly impact your cash flow, agility, and long-term growth.

The trick is to step back and look at what your business actually needs. Are you after flexibility, or are you investing in a core asset for the long haul?

An operating lease is all about agility. It helps you preserve precious capital and gives you access to the assets you need without the financial deadweight of ownership. Think of it as renting.

A finance lease, on the other hand, is for assets that are fundamental to your business—things you plan on using for most of their functional life. It’s less like renting and more like a financing plan for an eventual purchase.

When an Operating Lease Makes Sense

Think of the operating lease as your flexibility play. It’s a perfect match for a startup grabbing its first office, giving you the freedom to expand (or even downsize) without getting stuck in a rigid, five-year commitment.

This model is also a lifesaver for leasing technology that ages in dog years, like the laptops and servers a growing BPO needs to stay competitive.

Here are a few classic scenarios where an operating lease shines:

- Testing a New Market: Want to see if a new city is a good fit? Lease a small retail or office space to test the waters without betting the farm.

- Rapidly Evolving Needs: BPOs often have to scale their headcount and IT gear at a moment's notice. An operating lease lets them add or upgrade equipment on demand.

- Short-Term Projects: If you need a specialized piece of machinery for a six-month project, leasing it avoids the headache of buying it and then trying to sell it off later.

When to Choose a Finance Lease

A finance lease is your go-to when you're bringing in a foundational asset—something that’s absolutely critical to your long-term success. It’s a strategic acquisition that you’re essentially paying off over time.

If an asset is the engine of your revenue and you know you'll be using it for years, a finance lease acknowledges that reality. It puts the asset on your balance sheet, letting you build equity while keeping your cash flow predictable.

A great example is a manufacturing company acquiring a piece of mission-critical machinery or a logistics firm getting a new fleet of delivery trucks. These aren't temporary tools; they're the very foundation of the business.

This isn't just a local trend. Globally, Asia Pacific is becoming a major driver for finance lease growth. That market is projected to expand at an 8.1% CAGR, fueled by huge infrastructure projects and government policies that encourage asset financing. You can discover more insights about these global leasing dynamics.

Ultimately, it comes down to asking the right questions about your operational needs and your financial strategy. Whether you need the plug-and-play flexibility of an operating lease for a BPO workspace or the ownership path of a finance lease, the right choice is the one that fuels your business.

If you're exploring flexible office solutions that align with your growth plans, get in touch with our team to discuss your options.

Your Leasing Playbook for Sustainable Growth

The old lines between a capital lease and an operating lease have been completely redrawn. Getting a handle on this new landscape isn't just for the accounting department anymore—it's a critical skill for running your business smartly.

We’ve walked through how the new standards, ASC 842 and IFRS 16, now push almost every lease onto your balance sheet, demanding more honesty in how you report your finances. You’ve seen how this choice directly hits your P&L and balance sheet and, more importantly, how to pick the right path for where your business is headed.

The real takeaway here? The right lease is a powerful tool for growth. It’s how you get the assets you need to operate without draining your cash reserves, giving you the flexibility to pivot and build a business that can weather any storm.

Think of it this way: modern leasing isn't about finding a clever workaround. It's a clear strategic choice. Do you need temporary access to an asset (an operating lease), or are you on a path to eventually owning it (a finance lease)? Your answer writes a crucial chapter in your company's financial story.

Use this guide as your playbook. Move forward with the confidence that you’re not just signing a contract, but making a strategic decision that fuels your mission.

For more practical insights on building a rock-solid business, from operations to finance, check out the resources on the Seat Leasing BPO blog. By truly understanding these leasing concepts, you can turn what seems like a complex accounting headache into a major advantage for smart, sustainable growth.

Common Questions, Answered

Lease accounting can feel a bit like a maze, especially with the recent rule changes. Let's clear up some of the most common questions that pop up when businesses are trying to figure this all out.

So, What's the Real Difference Between a Capital and Operating Lease Today?

The biggest change under the new rules (think ASC 842 and IFRS 16) is that both lease types now land on your balance sheet. Whether you sign a finance lease (the new name for a capital lease) or an operating lease, you have to record a "Right-of-Use" asset and a lease liability. This was a huge shift from the old days when operating leases were kept off the books.

So where's the difference? It's all about how the expense shows up on your income statement.

- A finance lease gets split into two expense categories: interest and amortization. This usually means your expenses are higher at the beginning of the lease and taper off over time.

- An operating lease, on the other hand, is much simpler. It's recorded as a single, straight-line lease expense. The cost stays the same month after month, year after year, which makes budgeting a lot more predictable.

How Could a Finance Lease Mess With My Company's Loan Agreements?

This is a big one. Because a finance lease adds a hefty liability to your balance sheet, it can throw off the financial ratios your bank cares about. Things like your debt-to-equity or debt-to-asset ratios will instantly look worse, and that could trip a wire in your loan agreements.

It's absolutely critical to dust off those loan covenants and read the fine print before you sign a new finance lease. Have a conversation with your lender ahead of time to flag the potential impact. It's far better to renegotiate terms proactively than to explain a breach after the fact.

A quick chat can save you a world of headaches and keep your financing on solid ground.

Do Small Businesses Get a Pass on These New Accounting Rules?

Unfortunately, no. The whole point of these new standards was to create a level playing field, so the rules apply to just about everyone, regardless of size.

However, the rule-makers did throw small businesses a bone. There are a few practical shortcuts you can take to make life easier. The most popular one is an exemption for short-term leases, which are usually defined as anything 12 months or less. This means you don't have to go through the whole asset-and-liability song and dance for a simple, one-year rental.

Even with these shortcuts, the core rules are still in play. Your best move is always to talk to your accountant. They can help you navigate the options and lighten the compliance load for your specific situation.

At Seat Leasing BPO, we get that agility is everything. Our workspace solutions are built for businesses that need to move fast without being weighed down by complex, long-term commitments that clutter up the balance sheet. Discover how our flexible seat leasing model can work for you.