Long before you ever sit down across the table from a landlord, the most important work of your commercial lease negotiation has already begun. The secret to a great deal isn't just about sharp tactics in the moment; it's about building a rock-solid game plan. This prep work is what separates tenants who get favorable terms from those who end up with long-term financial headaches.

Building Your Negotiation Game Plan

Trying to negotiate a lease without a strategy is like sailing without a map—you’ll end up somewhere, but probably not where you intended. A good plan ensures every move you make is deliberate and directly serves your business goals.

The very first thing you need to do is get brutally honest about what you absolutely need versus what would be nice to have. This isn't just about square footage. It's about the nuts and bolts of what will make or break your operations and growth down the road.

Defining Your Must-Haves and Nice-to-Haves

Grab a pen and paper (or open a doc) and make two lists. The "must-haves" are your non-negotiables, the things that would make you walk away from a deal. The "nice-to-haves" are your bargaining chips—valuable perks you can trade during the negotiation.

- Location Essentials: Do you live and die by foot traffic? Is being near a major highway or public transit a must? What about proximity to your key clients or suppliers?

- Space and Layout: Sure, you need a certain amount of square footage, but what about the flow? An open-plan office is useless if you need private rooms. A great storefront doesn't help if you need a massive warehouse in the back. Get specific.

- Critical Amenities: Think about the infrastructure. Is high-speed internet a given? Is there enough parking for your team and customers? What about HVAC capacity or building security? Don't assume anything.

With this list in hand, you can start digging into market research. You need to know what similar properties are going for in your desired area. This data is your most powerful tool. When you can confidently say, "The building two blocks over is offering a lower rate and a better tenant improvement package," you suddenly have real leverage.

Assembling Your Professional Team

I've seen too many business owners try to go it alone, and it's a huge mistake. Landlords and their agents are pros; this is what they do all day. You need to even the playing field by having your own experienced team.

Your team is your greatest asset. A good broker finds the opportunities, and a sharp attorney protects you from the hidden liabilities. Overlooking either can cost you far more than their fees.

Make sure you have these two people in your corner:

- A Commercial Real Estate Broker: They know the market inside and out, have access to listings you'll never find on your own, and can act as your chief advocate and negotiator.

- A Real Estate Attorney: Their entire job is to pour over the fine print, spotting those tricky clauses that could sink your business years from now.

Timing is another massive piece of the puzzle. If you wait until the last minute, you're handing all the power to the landlord. They know you're desperate. The data doesn't lie: starting the conversation 12-18 months before your current lease is up gives you the most bargaining power and leads to much better deals. Once you're inside that six-month window, your options shrink, and the landlord knows it. You can find out more about how timing impacts negotiation leverage on our blog.

Finally, take a hard, conservative look at your finances to nail down a realistic budget. This isn't just the base rent. You have to factor in Common Area Maintenance (CAM) charges, utilities, insurance, and the potential costs for any build-out you need. Knowing your absolute top-dollar number will keep you from getting emotionally attached to a space that will bleed you dry. For more insights on managing operational costs, feel free to check out our other articles.

Decoding the Critical Lease Clauses to Negotiate

The commercial lease is where the real work begins. It's a dense legal document where a single sentence can empower your business or lock you into years of financial headaches. Getting comfortable with these key terms is the only way to negotiate a lease that genuinely works for you, not just the landlord.

Think of each clause as a lever you can pull. The right moves can translate into thousands of dollars in savings and give you the operational flexibility you need to grow. Let's dive into the most critical areas you absolutely must focus on.

To give you a bird's-eye view, here's a quick summary of the clauses we'll be breaking down and what your primary goal should be for each.

Key Commercial Lease Clauses and Negotiation Goals

| Lease Clause | What It Means | Tenant's Negotiation Goal |

|---|---|---|

| Rent & Escalation | The base rent and how it increases annually. | Secure a lower starting rent and cap future increases to a predictable, fixed percentage. |

| Lease Term & Renewal | The length of the initial lease and your right to extend it. | Get a shorter initial term with multiple renewal options at "fair market value." |

| Tenant Improvement (TI) | Landlord's financial contribution to your office build-out. | Maximize the TI allowance to cover both hard and soft construction costs. |

| CAM Charges | Your share of the building's operational costs. | Tightly define what's included, exclude capital expenses, and cap annual increases. |

| Termination & Subletting | Your options for getting out of the lease early. | Secure the right to sublet or assign the lease with reasonable landlord consent. |

Understanding these clauses is your foundation for a successful negotiation. Now, let's explore how to tackle them one by one.

Rent and Escalation Clauses

The base rent is the number everyone sees, but it's only the beginning of the story. Your negotiation can't stop there; you have to dig into the escalation clause, which dictates how and when your rent goes up.

Most landlords will propose annual increases, often a fixed 3% or a rate tied to the Consumer Price Index (CPI). This might sound standard, but it’s absolutely on the table for negotiation.

- Fixed Percentage: In a stable market, a fixed rate gives you predictability. Your job is to push for the lowest possible percentage.

- CPI-Based: Tying your rent to inflation is a gamble. If inflation skyrockets, your rent does too. Always, always fight for a cap on CPI increases to shield your budget from economic volatility.

I once worked with a startup that was offered a lease with CPI-based escalations. We managed to negotiate a 4% annual cap. When inflation later jumped to 7%, that one small change saved them tens of thousands of dollars over their five-year term.

Lease Term and Renewal Options

The lease term is a massive commitment. Landlords love long terms because it means stability for them. But as a tenant, you need flexibility. The sweet spot is a structure that gives you both.

A five-year term with two, five-year renewal options is a great target for most tenants. This setup gives you control of the space for up to 15 years without forcing you into a decade-plus commitment if your business pivots.

The real power isn't just in having the option, but in how the renewal rate is determined. Push for the renewal rate to be set at "fair market value," not some inflated, pre-set percentage. This ensures you're not locked into overpaying down the road.

Tenant Improvement Allowance

Let's be realistic: a commercial space is rarely move-in ready. You'll need to build offices, run data cables, or customize the layout. This is where the Tenant Improvement (TI) allowance comes in—it's the money the landlord gives you to fund the build-out.

The TI allowance is one of the biggest financial wins you can score. It's usually quoted per square foot (e.g., $40 per square foot). Your mission is to get this number as high as possible to reduce what you pay out of pocket.

Also, be crystal clear about what the TI covers. Does it include just "hard costs" like drywall and paint, or does it also cover "soft costs" like architectural drawings and permit fees? Nailing this down upfront will save you from major headaches later.

Common Area Maintenance Charges

Common Area Maintenance (CAM) charges cover your portion of the costs for maintaining shared spaces—lobbies, elevators, parking lots, you name it. If they aren't carefully defined and capped, CAMs can become a huge, unpredictable expense.

Here’s your CAM negotiation checklist:

- Demand a Detailed List: Insist on an itemized list of every single thing included in CAMs.

- Negotiate Exclusions: Argue to exclude capital expenditures. A new roof or HVAC system is the landlord's asset, not your operational expense.

- Cap the Increases: Just like with rent, negotiate a firm cap on annual CAM increases. A 5% cap is a reasonable starting point.

Unchecked CAMs can quickly sour a good deal. Getting this clause right is non-negotiable for a smart tenant.

Your Strategic Escape Hatches

The future is unpredictable. Your lease needs to reflect that by giving you options. Clauses covering termination, assignment, and subletting are your strategic escape routes if things don't go according to plan.

- Termination Clause: This defines how you can end the lease early. Landlords don't like giving these up, but you can often negotiate a termination right that comes with a penalty, like paying a few months' rent. It’s a much better alternative than being on the hook for the entire remaining term.

- Assignment and Subletting: An assignment clause lets you transfer the lease to another company if you sell your business. A subletting clause lets you rent out a portion (or all) of your space. Fight for language that says the landlord "cannot unreasonably withhold consent" to these requests. This gives you a lifeline if your business needs change.

Mastering Your Negotiation and Communication Skills

Knowing which lease clauses to target is only half the battle. The other, and frankly more critical half, is knowing how to actually ask for what you want and get it. The art of negotiation isn't about being pushy or confrontational; it’s about clear, confident, and strategic communication.

A good negotiation ends with both sides feeling like they won. Your aim is to create a situation where the landlord is genuinely happy to have you as a tenant, and you walk away with lease terms that will help your business succeed.

How to Use Competing Offers as Leverage

There's no tool more powerful in your negotiation kit than a competing offer from another building. It’s the single best way to prove your value as a potential tenant—by showing you have other real, viable options. This isn't about bluffing; it's about doing your due diligence and creating legitimate leverage.

Walking into a negotiation with a Letter of Intent (LOI) from another landlord completely changes the dynamic. The conversation shifts from, "What are you willing to give me?" to "Here's what the market is offering." This immediately creates a sense of urgency and frames you as a serious, well-informed prospect.

For example, you could say:

"We really like this space, but we have another offer on the table that includes a $50 per square foot tenant improvement allowance. For this to be a competitive option for us, we'd need you to match that."

Notice how that’s direct, based on data, and leaves emotion out of it. Your request becomes a simple condition for making a deal in a competitive market, not just a random demand.

Finding the Right Tone: Firm but Collaborative

Your tone from the very first email or phone call can set the stage for the entire negotiation. You have to strike a balance—be firm on your must-haves while staying collaborative on the points where you have some wiggle room. A landlord is far more likely to bend on key terms if they see you as a reasonable, long-term partner instead of an adversary.

- Ditch the ultimatums. Instead of "We won't sign without this," try framing it as a problem you can solve together. For instance, "For our business model to work here, we need to find a way to cap the CAM increases. How can we work together to make that happen?"

- Remind them of your value. Don't be shy about why you're a great catch. Casually mention your strong credit history, your company's track record of growth, or how your brand will elevate the building's tenant mix.

Scripts You Can Actually Use

It helps to have a few phrases in your back pocket to boost your confidence and keep the conversation on track. Here are a few lines I've seen work time and again when you negotiate a commercial lease.

For countering the first offer:

"Thanks for sending this over. We've reviewed the proposal and we're definitely excited about the potential here. To get this deal done, we’ll need to make some adjustments to the base rent and the TI allowance. Here’s what we had in mind…"

For asking for concessions:

"Given the current market and the length of the lease we're committing to, we were expecting to see a few months of free rent to help us offset our moving and build-out costs. That's been pretty standard in the other deals we're looking at."

For pushing back on a bad clause:

"The current language in the subletting clause is a bit too restrictive for our needs. We need the flexibility to adapt if our business grows faster than expected. We'd like to amend it to state that consent will not be unreasonably withheld."

Remember, the goal is to always keep the conversation moving forward. Every email and call should be a step toward a final agreement. Knowing when to push, when to be patient, and ultimately, when to walk away is the mark of a smart negotiator. Your preparation and communication skills are what will turn a standard lease into a strategic asset for your business.

Reading the Room: How Market Trends and Global Norms Shape Your Lease

To get the best possible deal on a commercial lease, you have to look beyond the four walls of the building and understand the bigger picture. The commercial real estate market is a living, breathing thing, constantly changing with the economy, new ways of working, and even global business customs. What worked for a tenant five years ago could be a terrible strategy today.

Without a doubt, the biggest shift we've seen is the explosion of hybrid and remote work. This isn't just a trend; it's a fundamental change in how companies think about office space. The days of needing a massive headquarters just to house every employee are largely over, and that creates some incredible opportunities for tenants who know what to ask for.

This has led to a major "flight to quality." Businesses are ditching mediocre spaces and instead looking for high-end, amenity-rich buildings that make coming to the office a genuine draw for their teams. It's less about raw square footage and more about the quality of the experience.

Smaller Spaces Mean Bigger Tenant Power

Companies everywhere are re-evaluating how much space they actually need. They've realized that a smaller, more thoughtfully designed office works just fine when you don't have the whole team in at once. This trend has put a real squeeze on landlords, especially those with large, traditional office blocks to fill.

And that, right there, is your leverage.

With office vacancy rates climbing in many cities, landlords are feeling the pressure. They're far more willing to negotiate and offer sweeteners to get a quality tenant in the door. Frankly, they need you more than you need any single one of them.

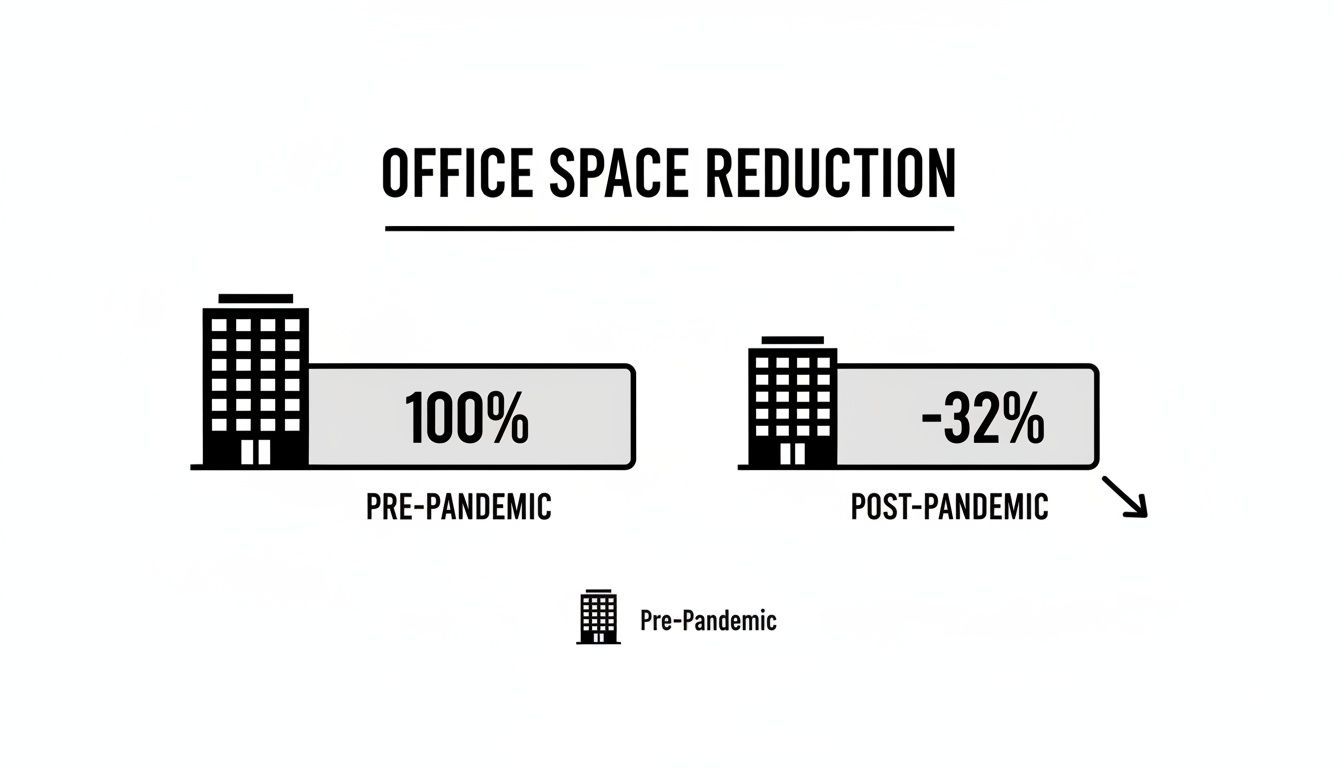

The numbers don't lie. In the U.S. market, for example, the average lease size is now 27% smaller than it was before the pandemic. Even more telling, brand new leases are showing a 32% drop in square footage. This is a clear signal that businesses are dodging long, expensive commitments. You can dig into more of these office leasing trends in recent market reports.

Today’s negotiation isn't just about the price per square foot. It’s about the total package. Use the current market softness to demand shorter terms, a hefty tenant improvement allowance, and the freedom to sublet if your needs change.

How Leasing Works Around the World

If your business is global—or has ambitions to be—you need to know that a lease negotiation in New York is a world away from one in London or Tokyo. Walking in with American-style expectations is a surefire way to hit a brick wall.

Here are a few examples I've seen play out:

- United Kingdom: Landlords here love stability, so they push for very long lease terms—think 10-15 years as a starting point, with rent reviews every five years. Your number one goal as a tenant is to negotiate a "break clause," giving you the option to exit the lease early.

- Asia (e.g., Japan, Singapore): Business here is often built on relationships. The negotiation process can feel less confrontational, but be prepared for hefty security deposits, sometimes as much as six months' rent or more. It’s seen as a sign of commitment.

- Europe (e.g., Germany, France): Many European countries have highly regulated rental markets that offer strong tenant protections. Leases are typically for a fixed term, but the laws around renewals and ending a lease can be complex and rigid.

These cultural and legal quirks completely change the game. This is where your local broker and attorney become your most valuable players. Adapting your strategy to local norms not only shows respect but dramatically increases your odds of landing a great deal, wherever you set up shop.

Rethinking the Traditional Lease: Is There a Better Way?

Sometimes, the best negotiation tactic is walking away from the table entirely—not out of spite, but because you've found a smarter alternative. For a growing number of businesses, especially in sectors like BPO, the old-school, long-term commercial lease just doesn't make sense anymore. It’s a rigid commitment in a world that demands flexibility.

This is where options like seat leasing come into play. Instead of chaining yourself to a five or ten-year financial obligation, you adopt a model that can grow (or shrink) right alongside your business. Think of it as a strategic pivot, trading a long-term liability for on-demand agility and much healthier cash flow.

The Hidden Burdens of a Conventional Lease

Anyone who has signed a traditional lease knows the base rent is just the beginning. The real costs—both in dollars and in headaches—are buried in the fine print and the day-to-day operational grind.

A conventional lease often means you're on the hook for a surprisingly long list of responsibilities that have nothing to do with your actual business.

- Massive Upfront Investment: You’re paying for everything. The entire build-out, the furniture, the cabling, the security system… it can easily run into tens or even hundreds of thousands of dollars before you ever move a single employee in.

- The Financial Straitjacket: That multi-year lease becomes a fixed anchor on your balance sheet. It doesn't care if you've had a record-breaking quarter or a challenging one. For companies in a growth phase, this lack of wiggle room can be a killer.

- The "Accidental Property Manager" Role: Suddenly, your team is juggling IT infrastructure, internet providers, utility companies, security vendors, and daily maintenance. Every minute spent dealing with a flickering light or a downed network is a minute you're not focused on serving your clients.

This model essentially forces you to run a second business as a property manager, a distraction most founders can't afford.

Seat Leasing: The Plug-and-Play Alternative

Seat leasing flips this entire script. Instead of renting an empty, cold shell of a space, you lease fully-equipped, ready-to-go workstations in a professionally managed environment. It's a true "plug-and-play" solution that wipes out nearly all the upfront costs and daily hassles.

The real power of a flexible workspace isn't just about the bottom line. It's about reclaiming your team's time, focus, and capital so you can pour those resources back into what truly drives your business forward.

With a provider like Seat Leasing BPO, the entire office infrastructure is part of the package. This goes far beyond just a desk and a chair. You get the mission-critical support that a modern office depends on:

- High-speed, redundant fiber internet

- On-site professional IT support

- All utilities (electricity, water, HVAC) included

- 24/7 building security and controlled access

- Daily janitorial and maintenance services

This all-inclusive approach rolls a dozen potential bills and vendor relationships into one clear, predictable monthly payment. For anyone trying to budget or forecast, that kind of simplicity is gold.

Traditional Lease vs. Seat Leasing Cost Comparison (Annual Estimate)

To really see the difference, let's look at the numbers. The table below provides a rough annual cost comparison for a small 20-person team, illustrating how quickly the "hidden" costs of a traditional lease add up.

| Cost Item | Traditional Commercial Lease | Seat Leasing BPO |

|---|---|---|

| Annual Base Rent | $72,000 | $48,000 |

| Upfront Build-Out (Amortized over 5 years) | $10,000 | $0 |

| Furniture (Amortized over 5 years) | $4,000 | $0 |

| Utilities (Electricity, Water, HVAC) | $8,400 | Included |

| Internet & IT Support | $9,600 | Included |

| Security System & Monitoring | $1,200 | Included |

| Janitorial Services | $4,800 | Included |

| Administrative Overhead (Management Time) | $5,000 | $0 |

| Total Estimated Annual Cost | $115,000 | $48,000 |

As you can see, the all-in cost of a traditional lease is often more than double the sticker price of the rent itself. Seat leasing provides a much more transparent and cost-effective path, freeing up significant capital that can be reinvested into growth.

This shift in thinking is already happening across the market. Companies are getting smarter about how they use office space, and the data proves it.

The market is seeing a 32% reduction in the average size of new office leases. This isn't a fluke; it's a strategic move away from the big, risky, long-term commitments of the past. For many, the best lease negotiation is choosing a model that doesn't require one at all.

Your Top Questions About Commercial Lease Negotiation, Answered

Even with a solid game plan, let's be honest—diving into commercial real estate can feel like a lot. Most business owners I talk to have the same core questions when they're staring down their first lease negotiation. Getting some straight answers can take the whole process from intimidating to manageable.

So, I've pulled together some of the most common questions that pop up. These are based on the typical sticking points and the areas where a little bit of know-how can make a massive difference in the deal you end up with.

How Much Can You Really Shave Off a Commercial Lease?

Everyone wants to know the magic number, but there's no universal discount. How much you can negotiate really comes down to the local market. Is it a tenant's market overflowing with "For Lease" signs, or is it a landlord's market where you have to fight for a good spot?

Instead of getting hung up on a specific percentage off the rent, I always advise clients to focus on the high-value concessions that reduce their total cash outlay.

- Free Rent: This is a big one. A good starting point is to ask for one month of free rent for every year of the lease term. So, on a five-year lease, you’d shoot for five months free. It's a common and incredibly valuable win.

- Tenant Improvement (TI) Allowance: This is literally the landlord's cash to help you build out your space. Pushing for a higher TI allowance directly lowers how much you have to pay out-of-pocket to get the doors open.

The real victory isn't just a lower base rent. It's the total value of the deal, which includes these concessions, limits on your expenses, and flexible terms. You might find that a slightly higher rent is an amazing deal if the landlord is footing the bill for a huge TI allowance.

What’s the Single Most Important Clause to Get Right?

This is a tough one because every clause matters, but if I had to pick, I'd say the "Use" and "Subleasing/Assignment" clauses are the most critical for your long-term health. Think of these two as your strategic safety net.

A restrictive 'Use' clause can choke your ability to innovate or pivot, while a tough 'Subleasing' clause can trap you in a space you no longer need. Negotiating broad rights in these areas protects your business against unforeseen changes.

Picture this: your business model evolves in a couple of years. A narrowly defined "Use" clause could stop you from adding a new, profitable service. On the flip side, if you suddenly need to downsize or even relocate, a flexible "Subleasing" clause is the lifeline that keeps you from paying for an empty office.

Do I Really Need a Lawyer to Look at This?

Yes. Full stop. This is not the place to cut corners.

Your commercial broker is your expert for finding the space and hammering out the business terms. But a specialized real estate attorney is your last line of defense against the risks buried in the legal jargon of that 50-page document.

They are trained to see what you can't.

- They'll spot ambiguous language that could turn into a costly dispute down the road.

- They make sure all those things you agreed to verbally actually made it into the final contract correctly.

- They protect you from long-term liabilities that could be financially devastating.

The fee you pay a lawyer upfront is a tiny investment compared to the crushing cost of a bad lease. It’s some of the best business insurance you can buy.

For businesses that would rather skip this entire maze, an all-inclusive alternative like Seat Leasing BPO can be a game-changer. You avoid long-term commitments and huge upfront costs, getting a fully serviced workspace ready for your team on day one. If you're looking for a smarter way to handle your office needs, you can learn more about our model.